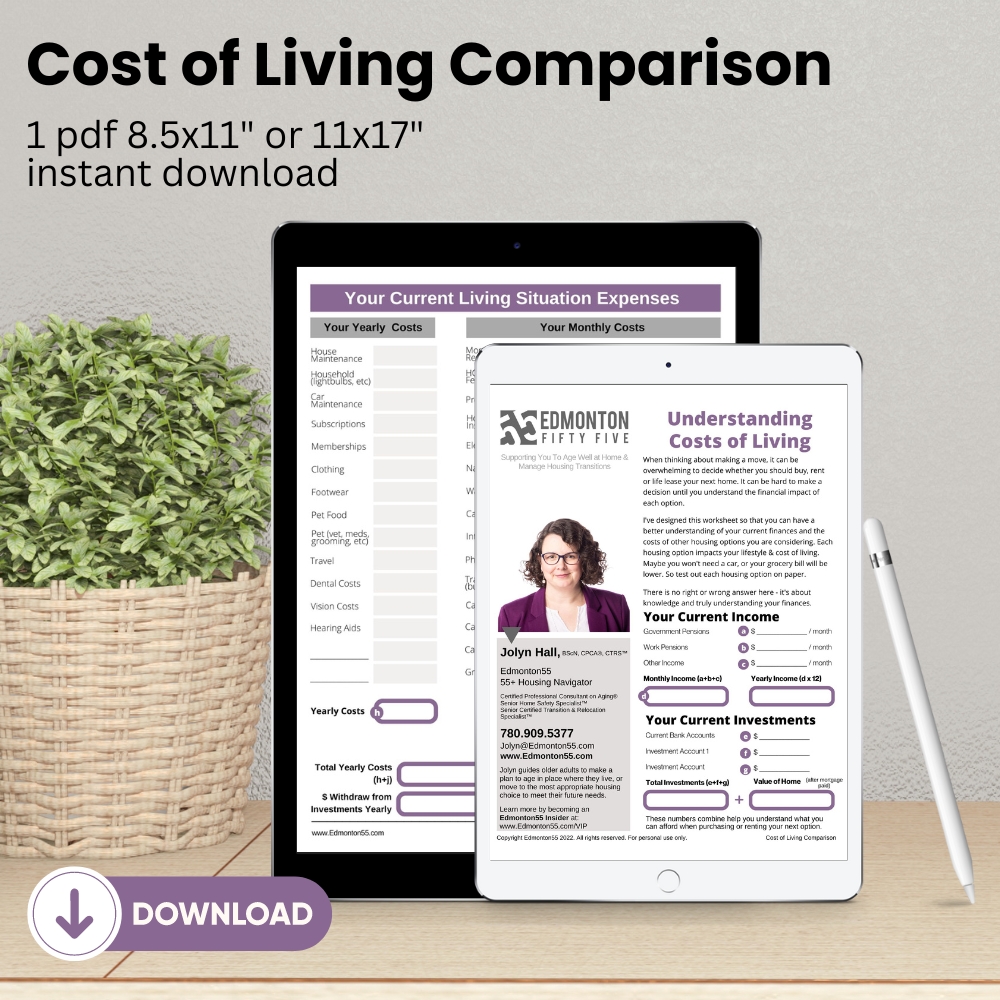

Figuring out how to finance retirement living, can feel very expensive – especially if you have been living mortgage free in your home. Understanding different ways you can manage your finances, with a higher monthly rent than you are used to, is an early first step in planning your move.

Consult Your Financial Advisor

Your financial advisor can help you understand how your current income from pensions and investments, can work to fund your retirement living options. They might walk you through similar suggestions you’ll see below, or confirm what monthly rent range you should try to keep your costs within. Their fancy computer programs will show you exactly how long you could live in that retirement living option for, before your money runs out. They can give you peace of mind, and a strategy to manage your money in a way to support the lifestyle and potential care needs you may require.

If you don’t have a financial advisor, if you are a VIP member, you can see my list of preferred financial advisors and financial planners here: VIP VENDOR DIRECTORY

Sell or Refinance Your Home

So many times, older adults are just looking at their monthly income, instead of looking at their income + equity they have in their home. Especially if you are mortgage free or a low mortgage on your home, you have a couple of options.

If you are thinking you want to move into retirement living first, make sure you like it, and then sell your home – you can apply for a home equity line of credit (HELOC). This is based on the appraised value of your home and you are given a line of credit to use whenever you are ready. You can use this towards your monthly costs of retirement living until your home is sold, or to help with moving expenses and even just peace of mind the money is there is you need it. The best part is most plans do not require monthly payments, you simply pay back the line of credit when you do decide to sell your home. Your bank or a mortgage broker can help you with this option, but a HELOC traditionally takes about 6 weeks to set up – so start this process well before you need to make a move to retirement living.

Selling your home can feel overwhelming and daunting – but with the right team of downsizers, move managers and moving companies – it can be an easier process than expected. Selling your home and then moving into retirement living, allows you to use and/or invest the money from the sale of your home to help with the costs of retirement living. If you have already selected a suite at a retirement residence, you can give a relatively short possession time to potential buyers – which many will appreciate. Be sure to get a market evaluation from a Seniors Real Estate Specialist who can assist you with all the elements that go into selling your last home.

If you don’t have a mortgage brokers or real estate professionals, if you are a VIP member, you can see my list of preferred mortgage brokers and real estate agents here: VIP VENDOR DIRECTORY

Subsidized Housing Options

If your income does not give you the ability to pay for retirement living rent – which can often be over $2500/month – then you might have to see if you qualify for subsidized housing options. These options are often restricted to those who make less than $35,000 per year as an individual or under $48,000 as a couple. These will not have as much space or as many amentities & activities as you might see in private retirement living options. There are subsidized senior apartments (with no services) and subsidized lodges (with support services such as meals, housekeeping & activities). Many of these residence types have quite long waitlists, so be prepared to wait 6 months to 3 years depending on the residence. Another reason why it is essential to plan your future housing options early. There is no option for urgent placement if your needs suddenly change and you can’t stay at home. Monthly fees are often 30% of your income, if you qualify for this housing type.

Subsidized Care Options

If you require more home care than what can be offered in the home, you may want to move to the Alberta Health Services Supported Living Program. You must be receiving homecare, and you must be receving more advanced care (generally unscheduled care needs) to qualify for this program. Once your Home Care Case Manager has determined your qualify for this type of housing, you’ll be presented with a list of retirement living residences that have rooms dedicated to the Supported Living Program. You will choose 3 residences you want to be considered for, then you’ll be put on a waitlist. You’ll be matched when the first of the 3 options comes available. Waittimes can vary quite a bit, often in the 6-9 months range, again this is not a quick option and requires some advance planning. You’ll need to move in within 72 hours, so having the home ready to sell or starting to downsize in advance is important. Monthly rental fees are often around $2100/month in this program.

Starting with Private Housing then to Subsidized Housing

If you could benefit from subsidized options, but can’t wait for space to come available – there is an option. Some choose to pay for private retirement living first, so that they can get the care and support quickly they need, as many residences have 1-2 month waitlists. Then, if you qualify for subsidized housing or the supportive living program, you can get your name on that waitlist. This means that you are paying for private retirement living usually for a year or less, until space becomes available to you in subsidized options. This isn’t a great option, as it means making two moves. But if you just can’t remain in your home and can’t endure a lengthy waitlist, this is the option you may need to consider. Be sure to be upfront with your retirement living residence about your plans to move to subsidized living, so you are fully away of termination of lease requirements before you move in.

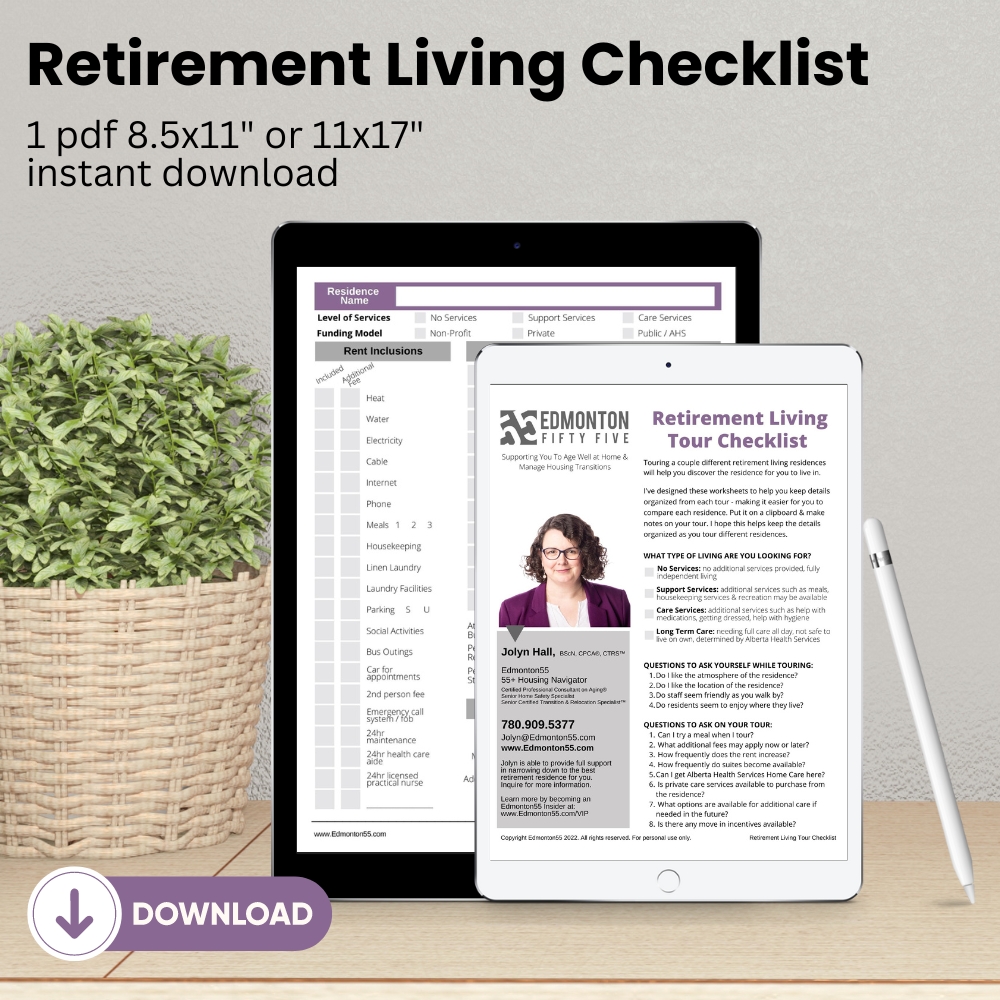

5 Creative Ways to Reduce Your Monthly Rent Costs

I just want to quickly touch on a couple of ideas that might help you find a retirement living option that best fits your budget.

- Choose a smaller room – either less square footage or instead of a two bedroom, take a one bedroom suite. Be sure to explore the monthly costs of a couple different room types.

- Choose less services – generally speaking, a building with 1 meal a day will cost less than one that includes 3 meals a day. Exploring to find residences that start with less services than you need, means you can have lower costs until you need those additional services. Then you can add the extra services only when you need it.

- Be Open to different areas – if you have lived on the Soutside of Edmonton, you’ll know that often costs of retirement living might be higher than looking in the Northwest of Edmonton. Explore areas beyond your comfort zone as you might find some options you never thought about, that could be more affordable to you.

- Ask about what rooms are hard to rent – they might not have a stellar view or are a unique floor plan, but often these rooms might have a promotional rate to encourage them to be rented. These rooms aren’t generally shown on a standard tour, so be sure to ask if there is something harder to rent that has a possible reduced price. If you can manage that view or floor plan, it could be a great way for you to lower your costs.

- Be sure to ask about promotions – you just never know what deals there might be to cover parking costs or one month free, etc. Any of those promotions could be beneficial as you explore and decide the right retirement living option for you.

Sometimes talking about how to finance retirement living plans, and evaluating your current monthly costs and projected future costs can help you better plan for what option is best suited to you. By being empowered to do your research and plan which financial option best suits you, will help you be pro-active in planning your future housing needs.